As of May 2026, Microsoft (MSFT) is highlighted as the most promising AI stock due to its exceptional growth, strategic depth, and diversified AI portfolio spanning cloud, enterprise, and consumer applications. Other strong contenders include Intel (INTC), specializing in AI inference; CoreWeave (CRWV), a pure-play AI infrastructure provider; and tech giants Alphabet (GOOGL) and Meta (META), leveraging AI for growth and advertising. Additionally, Micron (MU) and SanDisk (SNDK) are crucial in AI memory hardware, while UiPath (PATH) and SentinelOne (S) offer targeted AI software exposure. Investors can also consider ETFs like AIQ for diversified exposure.

As of May 2026, Microsoft (MSFT) stands out as the most promising AI stock, driven by robust revenue growth (18% year-over-year in Q3 FY26), deep integration of AI across its Azure cloud and Copilot applications, and strategic investments in OpenAI. Its diversified ecosystem provides stability and creates strong network effects, positioning it for continued leadership in the enterprise AI market.

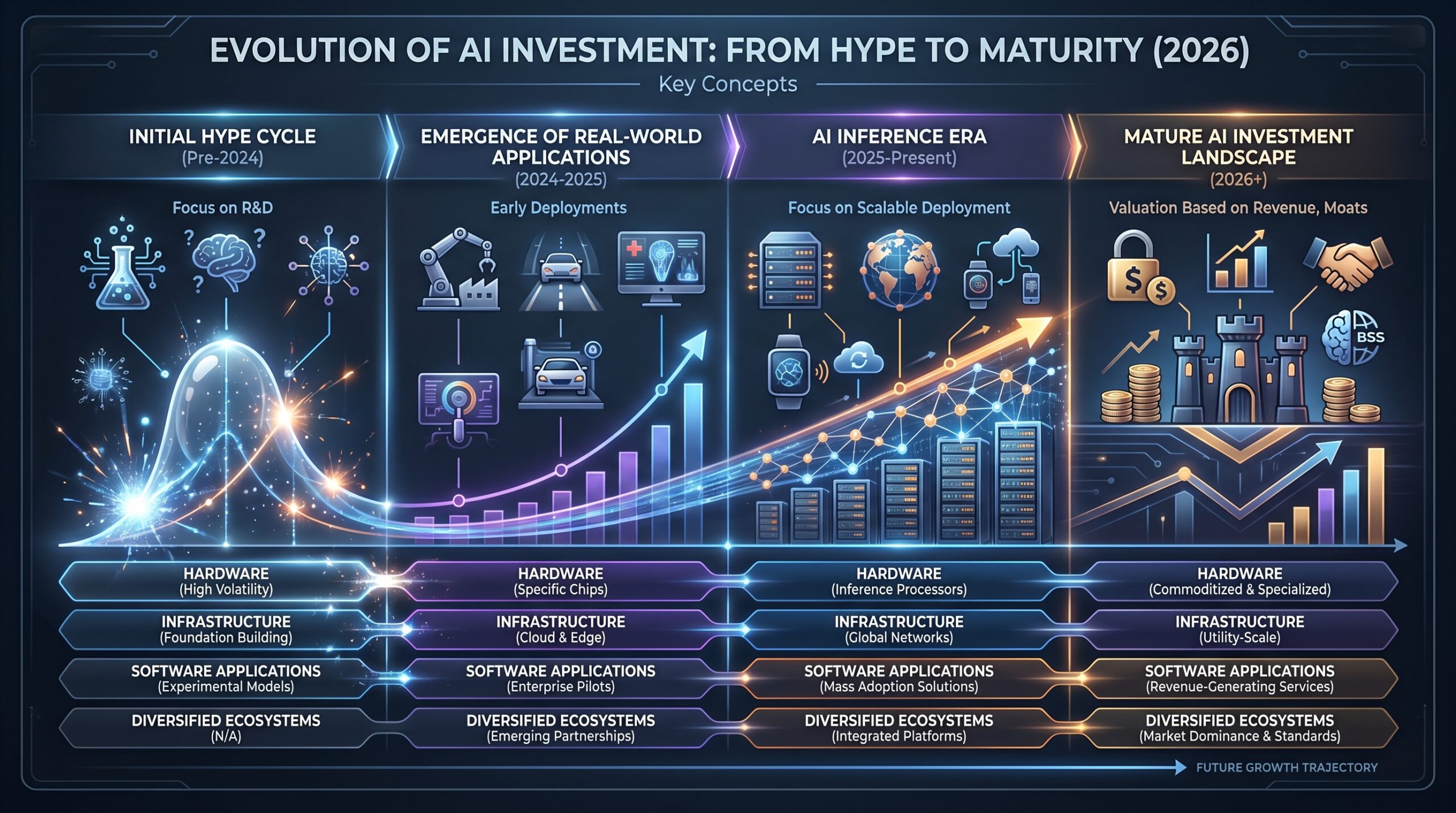

Defining the AI Investment Landscape in 2026

The AI investment landscape in 2026 is characterized by maturity, moving beyond initial hype cycles to focus on tangible revenue generation. Companies are now valued based on their integration of AI into core business functions and the strength of their competitive moats. The market has distinctly segmented into several critical categories, including foundational hardware (chips, memory), infrastructure (cloud, platforms), specialized software applications (such as agentic AI and cybersecurity), and diversified conglomerates that leverage AI across their vast ecosystems.

Success increasingly hinges on real-world deployment, marking the beginning of the "AI Inference Era" rather than just model development. This shift significantly benefits companies that provide inference-optimized chips, specialized cloud computing resources, and products that directly enhance enterprise efficiency or end-user experiences. For further insights into the broader AI landscape, consider “The State of AI in 2026: Read the Signal, Not Just the Headlines.”

Pure-play AI stocks, like CoreWeave, generate nearly all their revenue from AI-specific services, offering a concentrated investment. In contrast, diversified giants such as Microsoft use AI as a powerful growth accelerant across existing multibillion-dollar product lines. Investors must carefully distinguish between companies building AI tools (e.g., chipmakers) and those deploying them at scale (e.g., Meta’s advertising systems), as their risk profiles and growth drivers differ significantly.

Microsoft (MSFT): The Enterprise AI Juggernaut

Microsoft exemplifies how an established tech giant can not only adapt but dominate the AI era. Its fiscal Q3 2026 results, ending March 31, reported revenue of $82.9 billion, an impressive 18% year-over-year increase, with AI significantly fueling this growth. Azure and other cloud services saw substantial expansion, with AI specifically contributing approximately 7 percentage points to this overall growth. On April 30, Bernstein analyst Mark Moerdler reinforced confidence by raising Microsoft’s price objective to $646 from $641, maintaining an ‘Outperform’ rating.

Microsoft’s strength lies in its full-stack integration, covering infrastructure (Azure AI supercomputing), models (via its partnership and investment in OpenAI), and ubiquitous applications (Copilot embedded in Windows, Office 365, GitHub). This comprehensive approach creates powerful network effects, as enterprise customers adopting Microsoft 365 automatically gain access to advanced AI tools, securing recurring revenue streams. This strategy helps differentiate it in a competitive market, similar to how “Best AI Agents for Developers in 2026” discusses full-stack capabilities.

Its robust ecosystem approach effectively mitigates risk. While pure-play AI companies depend entirely on AI demand, Microsoft’s diverse revenue portfolio—encompassing cloud services, productivity software, and gaming—provides a stable foundation. AI integration enhances the value of these existing products, leading to higher customer retention and increased pricing power. The primary challenge remains its sheer scale; sustaining such high growth rates becomes mathematically more difficult as its annual revenue base expands beyond $300 billion.

Intel (INTC): The Emerging Inference Leader

Intel is undergoing a significant transformation, strategically positioning itself as a primary beneficiary of the "AI Inference Era." As of May 7, 2026, its stock performance has been surging, with analysts from firms like The Motley Fool suggesting it could potentially surpass even Nvidia and Broadcom in this specific domain. This dramatic shift highlights the critical importance of specialized hardware once AI models are developed.

AI inference refers to the process of applying a trained AI model to make real-world predictions or decisions. While Nvidia GPUs have historically dominated the training phase (teaching AI models), inference can often be run on different, more specialized, or cost-effective hardware. Intel’s Gaudi accelerators and next-generation Core Ultra processors, which feature dedicated AI NPUs (Neural Processing Units), are specifically designed to capitalize on this massive deployment wave. For a deeper dive into performance considerations, see “How Does TensorRT Affect Model Accuracy.”

Intel’s advantage is rooted in its profound manufacturing expertise and extensive enterprise relationships. Companies looking to deploy AI at the edge—on PCs, within factories, or in proprietary data centers—often prefer Intel’s x86 architecture compatibility and its comprehensive suite of software tools, such as OpenVINO. This strategically positions Intel to capture significant value as AI deployments transition from centralized cloud environments to pervasive, distributed computing. Such developments are crucial as discussions around “The On-Device AI Shift” intensify.

CoreWeave (CRWV): The Pure-Play AI Infrastructure Bet

CoreWeave represents a direct, high-risk, and high-reward investment in the foundational infrastructure of the AI revolution. It operates as a pure-play AI cloud provider, meaning its platform was specifically engineered for AI workloads, predominantly GPU-based compute, and it derives the vast majority of its revenue from this sector. Its impressive client list includes major AI players like Nvidia, OpenAI, Microsoft, and Meta. NVIDIA Corning AI Infrastructure Manufacturing provides context on the broader supplier market.

Unlike generalized cloud providers such as AWS, Google Cloud, and Azure, CoreWeave is optimized for performance and cost-efficiency in massive AI model training and inference. This specialization attracts customers who demand maximum GPU uptime, high-speed interconnects, and specialized software stacks. Its business model thrives on the explosive demand for compute power, positioning it as a "picks and shovels" play across the entire AI industry.

Investing in CoreWeave offers concentrated exposure to the AI infrastructure market. Its success is directly tied to the sustained and strong demand for AI compute cycles. While this demand is booming in 2026, the company could be vulnerable to any industry-wide slowdown or a significant technological shift that reduces the need for massive computational power, such as algorithmic breakthroughs in efficient training.

Alphabet (Google): A Growth and Value Hybrid

Alphabet demonstrates that AI leadership can coexist with a reasonable valuation in the current market. The company reported a 22% year-over-year increase in revenue, coupled with a remarkably high operating margin of 36%. Despite this robust performance, its forward P/E ratio hovers around 29, which is considered reasonable for a growth company of its caliber in the current market. This positions Google as a compelling AI investment, similar to the discussions in “Grokarium: What Is It? A 2026 Explainer” regarding new AI model valuations.

Google’s AI strength is multifaceted and deeply integrated across its services. Its Gemini AI models directly compete with offerings from OpenAI, illustrating its commitment to foundational AI research and deployment. The core search advertising business is being significantly augmented and protected by AI-powered search experiences, such as the Search Generative Experience (SGE). Furthermore, Google Cloud remains a top-tier platform for AI development and deployment, while YouTube leverages AI extensively for content recommendations and targeted advertising.

This diversification makes Alphabet a resilient AI investment. It monetizes AI through its own high-margin products, particularly advertising, and also sells AI tools and services to other businesses via Google Cloud. The primary risk remains competitive pressure in both the search and cloud markets, but its massive cash flows provide ample resources to continually innovate and invest in cutting-edge AI technologies.

Meta Platforms (META): AI at Scale for Advertising

Meta Platforms excels in applying sophisticated AI infrastructure to an immensely profitable use case: digital advertising. While often associated with the broader "generative AI" trend, Meta’s significant investment is in building advanced systems that more effectively target and personalize advertisements across its vast platforms, including Facebook, Instagram, and WhatsApp. For context on Meta’s broader AI strategy, consider “Zuckerberg’s Personal Approval of Meta’s AI Copyright Infringement.”

Meta’s massive datasets on user behavior feed highly advanced AI models that predict engagement and conversion rates with remarkable accuracy. This leads to a higher return on ad spend for marketers, which in turn allows Meta to command premium advertising prices. The company’s unwavering commitment to AI is evident in its substantial capital expenditures, which are heavily directed towards AI-optimized data centers and computing hardware.

For investors, Meta offers a clear narrative: AI directly drives its core revenue engine. This represents a more tangible and immediate application of AI compared to many speculative generative AI projects. The primary risk factors for Meta include its dependency on the cyclical nature of advertising spend and ongoing regulatory scrutiny concerning data privacy and content moderation.

Micron (MU) & SanDisk (SNDK): Owning the AI Memory Bottleneck

High-Bandwidth Memory (HBM) and advanced NAND flash are critical, yet often overlooked, components of high-performance AI systems. Both Micron and the recently spun-off SanDisk (SNDK) are pivotal players in this space. Micron’s stock has seen impressive gains in 2026, with some analysts, citing exponential earnings growth, suggesting it "could double by year-end."

SanDisk’s trajectory provides a concrete example of this demand. MoneyFlows data from June 2025 showed heavy institutional buying activity when SNDK was trading at approximately $106. This buying momentum continued, propelling the stock past $600 by May 2026. This significant surge reflects the skyrocketing demand for high-performance memory, essential for AI servers and advanced training clusters.

Investing in memory stocks is essentially a play on hardware scarcity and the increasing performance demands of AI. The performance of leading AI accelerators from Nvidia, Intel, and AMD is directly tied to the speed and capacity of their accompanying memory. As AI models continue to grow larger and more complex, this demand only intensifies. However, these stocks are highly cyclical and sensitive to industry supply and demand dynamics, making them inherently more volatile than diversified tech giants.

UiPath (PATH): Automating Enterprises with Agentic AI

UiPath has evolved from a leader in Robotic Process Automation (RPA) into a comprehensive AI-powered automation platform. In 2026, it significantly expanded its portfolio to include agentic AI solutions tailored for specific industries. The company received recognition across five G2 software award categories this year, notably including Best Agentic AI Software Products. This growth aligns with trends discussed in “Agent Island: New Benchmark for Agentic AI Progress.”

UiPath’s applications span critical areas such as healthcare revenue cycle management, procurement finance, and financial crime compliance, demonstrating a highly focused strategy. Instead of selling generic AI, UiPath develops intelligent agents that automate complex, multi-step workflows within established enterprise departments. This approach delivers clear, measurable return on investment (ROI) on software licensing costs, making it attractive to businesses.

UiPath’s AI strategy is fundamentally practical and ROI-driven, which strongly resonates with businesses operating in uncertain economic climates. Its growth trajectory is directly tied to the broader expansion of automation adoption within large enterprises. The primary risks include intense competition from larger platforms, such as Microsoft Power Automate, and the continuous need to justify the value of its specialized agentic solutions against more generalized AI tools.

SentinelOne (S): The Underrated AI Cybersecurity Play

SentinelOne represents a potentially undervalued opportunity within the AI-powered cybersecurity sector. The company was founded with AI at its core, utilizing advanced behavioral analysis to detect and respond to cyber threats. In its fiscal 2026 fourth quarter, it successfully increased its Annual Recurring Revenue (ARR) by 22% and, crucially, reported positive free cash flow of $51.9 million for the full fiscal year, even while still recording a net loss in Q4. For insights on AI’s role in security, refer to “IMF Warns: AI-Powered Threats to Global Financial Stability are ‘Inevitable’.”

This combination of strong growth and improving financial health is particularly noteworthy. Its Price-to-Sales (P/S) ratio of 5 is relatively low compared to many high-growth SaaS companies, suggesting that Wall Street may be undervaluing its significant progress. As cyber threats become increasingly sophisticated and pervasive, the demand for AI-native defense systems is only expected to grow.

The cybersecurity market is fiercely competitive, with industry giants like Palo Alto Networks and CrowdStrike also making substantial investments in AI. SentinelOne must continue to execute flawlessly to maintain its impressive growth rate and effectively differentiate its technology in this crowded field. The ongoing “AI News Roundup, 2026-05-07” often highlights competitive movements in this space.

Investing Through ETFs: The Diversified Approach

The Global X Artificial Intelligence & Technology ETF (AIQ) offers a practical way to invest in a diversified basket of AI companies, thereby mitigating the specific risks associated with betting on a single stock. With over $6 billion in assets under management, this ETF tracks an index of firms actively involved in the development and utilization of artificial intelligence technologies.

This instrument is ideal for investors who believe strongly in the long-term AI thematic but may lack the time or specialized expertise to thoroughly analyze individual companies and their intricate technologies. It provides instant diversification across various segments, including hardware, software, and services. The primary drawback is dilution; the gains of top-performing constituent companies are partially offset by weaker holdings, and the fund charges an expense ratio (management fee), which slightly reduces returns compared to purchasing individual stocks directly.

AI Investment Strategy Matrix

- Diversified Giant (e.g., MSFT, GOOGL, META): Best for risk-averse growth investors. Offers stable revenue and diverse income but slower growth potential due to size.

- Pure-Play Infrastructure (e.g., CRWV): Best for high-risk/high-reward speculators. Provides direct, concentrated exposure to AI demand but vulnerable to industry downturns.

- Hardware & Semiconductors (e.g., INTC, MU, SNDK): Best for investors understanding tech cycles. Critical, high-demand components but highly cyclical and volatile.

- Software Applications (e.g., PATH, S): Best for growth investors seeking specialization. High margins and scalable products but faces fierce competitive landscapes.

- ETF (e.g., AIQ): Best for hands-off, thematic investors. Offers instant diversification and lower single-stock risk but diluted returns and management fees.

| Investment Strategy | Best For | Example Tickers | Key Advantage | Key Disadvantage |

|---|---|---|---|---|

| Diversified Giant | Risk-averse growth investors | MSFT, GOOGL, META | Stable revenue, diverse income streams | Slower growth potential due to large size |

| Pure-Play Infrastructure | High-risk/high-reward speculators | CRWV | Direct, concentrated exposure to AI demand | Vulnerable to industry downturns |

| Hardware & Semiconductors | Investors understanding tech cycles | INTC, MU, SNDK | Critical, high-demand components | Highly cyclical and volatile |

| Software Applications | Growth investors seeking specialization | PATH, S | High margins, scalable products | Fierce competitive landscape |

| ETF (Diversified) | Hands-off, thematic investors | AIQ | Instant diversification, lower single-stock risk | Diluted returns, management fees |

Critical Risks in AI Stock Investing

Investing in AI stocks comes with significant perils that savvy investors must acknowledge when developing any investment strategy. The landscape is dynamic, and understanding these risks is paramount to making informed decisions. The rapid pace of change in AI can be both an opportunity and a threat.

Rapid Technological Obsolescence

The AI field evolves at a breakneck pace. A company that leads in a specific chip architecture or model type today could be rendered irrelevant by a new breakthrough tomorrow. This risk is particularly pronounced for pure-play hardware companies that rely heavily on specific technological advantages. “The Best AI Models of 2026” further illustrates this rapid change.

Intensified Competition

The massive potential rewards in AI have attracted countless competitors into almost every segment of the market. This intense competition can lead to price wars, significant margin compression, and market fragmentation, making it exceedingly difficult for any single player to maintain dominance long-term. This competitive pressure demands ongoing innovation and strategic differentiation.

Regulatory Scrutiny

Governments worldwide are actively examining AI’s extensive impact on privacy, data security, employment markets, and broader market power dynamics. New regulations could impose limitations on data usage, introduce substantial compliance costs, or even restrict specific AI applications, directly impacting companies’ revenue models and operational freedom. For example, “Deep Vision Fails in Scientific Imaging” touches on ethical considerations that often lead to regulations.

Valuation Bubble

Enthusiasm surrounding AI can often decouple stock prices from fundamental business metrics. A company trading at a P/E ratio of 100 based solely on ambitious future AI expectations is extremely vulnerable to a sharp correction if its projected growth does not materialize as quickly or as substantially as predicted. This points to the need for rigorous valuation analysis.

Economic Sensitivity

Many AI stocks fall into the category of growth stocks and are therefore more sensitive to macroeconomic conditions, interest rate hikes, and economic recessions than value stocks. During periods of economic uncertainty, investors tend to flee riskier assets, which can lead to significant volatility and downward pressure on these high-growth AI stocks.

Common Mistakes Investors Make

Chasing Headlines

A common pitfall is buying a stock solely because it garners positive AI news headlines, without conducting a thorough analysis of its financials, competitive position, or valuation. This impulsive behavior often leads to poor investment decisions based on hype rather than fundamental strength.

Ignoring Valuation

Assuming that "AI" automatically equates to growth at any price is a significant mistake. Paying an exorbitant P/E or P/S ratio for a company with unproven profitability or an unsustainable business model is a frequent way for investors to incur substantial losses. Valuation discipline remains crucial, even in rapidly growing sectors.

Overlooking the “How”

Failing to understand how a company generates revenue from AI is another common error. Many firms use AI internally to improve efficiency (a cost-saving measure) rather than selling AI products or services (a revenue-generating function). The latter typically offers more direct investment value. Understanding this distinction is vital for accurate assessment.

Lack of Diversification

Placing a disproportionate amount of capital into just one or two highly speculative AI stocks is a high-risk strategy. Thematic investing in AI should be a balanced component within a broader, diversified portfolio, not the entire portfolio itself, to manage risk effectively.

Confusing Hype for Substance

A company’s marketing department labeling every product "AI-powered" does not automatically qualify it as a leading AI stock. Investors must scrutinize the actual role of AI technology within the product and its direct contribution to the company’s revenue stream. Substance, not just branding, is key.

Myths and Misconceptions About AI Stocks

Myth 1: All AI stocks are created equal.

Reality: The AI ecosystem is vast and diverse. A memory chip manufacturer like Micron, a specialized cloud provider such as CoreWeave, and a software automation company like UiPath operate with vastly different business models, face distinct risks, and are driven by unique growth catalysts. Understanding these differences is crucial for effective investing.

Myth 2: NVIDIA is the only AI chip stock that matters.

Reality: While NVIDIA has been a dominant force in AI model training, the inference phase of AI is creating new opportunities and winners. Intel’s resurgence in 2026, driven by its focus on inference hardware, directly challenges this notion, proving that other players can capture significant value in the evolving AI chip market. This evolving landscape is also relevant for discussions on “AI on Android” and localized processing.

Myth 3: Old tech companies can’t compete with AI startups.

Reality: Microsoft, Google, and Meta serve as prime examples of how established giants, with their vast resources, extensive datasets, and deeply entrenched customer relationships, can effectively leverage AI to accelerate growth and fend off aggressive competition from newer startups. Their scale and existing infrastructure provide significant competitive advantages.

FAQ

- What is the most promising AI stock for long-term growth?

- Microsoft (MSFT) is a top candidate for long-term growth due to its diversified revenue streams, deep integration of AI across its product suite, and strong financial performance. Its extensive enterprise presence provides stability, while its AI innovations in Azure and Copilot drive significant new growth opportunities.

- Is it too late to invest in AI stocks in 2026?

- It is not too late, but the investment approach must be more selective and focused. The initial wave of speculative hype has largely subsided, forcing investors to focus on companies with proven revenue, sustainable profits, and clear competitive advantages rather than just future potential.

- What is a pure-play AI stock?

- A pure-play AI stock is a company whose primary business and nearly all revenue are derived from AI-related products, services, or infrastructure. CoreWeave is a prime example, as its specialized cloud platform is designed exclusively for AI workloads.

- Why is Intel considered a promising AI stock now?

- Intel is considered a promising AI stock due to its strategic positioning in the "AI Inference Era." Its Gaudi accelerators and client CPUs with integrated NPUs are specifically designed for efficiently deploying AI models, a critical and rapidly growing market segment where it can significantly challenge NVIDIA’s historical dominance.

- Are there any undervalued AI stocks?

- SentinelOne (S) may be considered undervalued based on traditional metrics. It has demonstrated strong ARR growth (22% in Q4 FY26) and achieved positive free cash flow, yet it trades at a relatively low Price-to-Sales (P/S) ratio of 5 compared to many other software growth stocks. This suggests the market may not yet fully appreciate its financial and technological progress.

- How do I invest in AI without picking individual stocks?

- The Global X Artificial Intelligence & Technology ETF (AIQ) provides a diversified basket of companies involved in artificial intelligence. This offers broad exposure to the overarching AI theme without the concentrated risk associated with the performance of any single company.