US China AI Competition Update: Direct Answer

The Narrowing AI Performance Gap

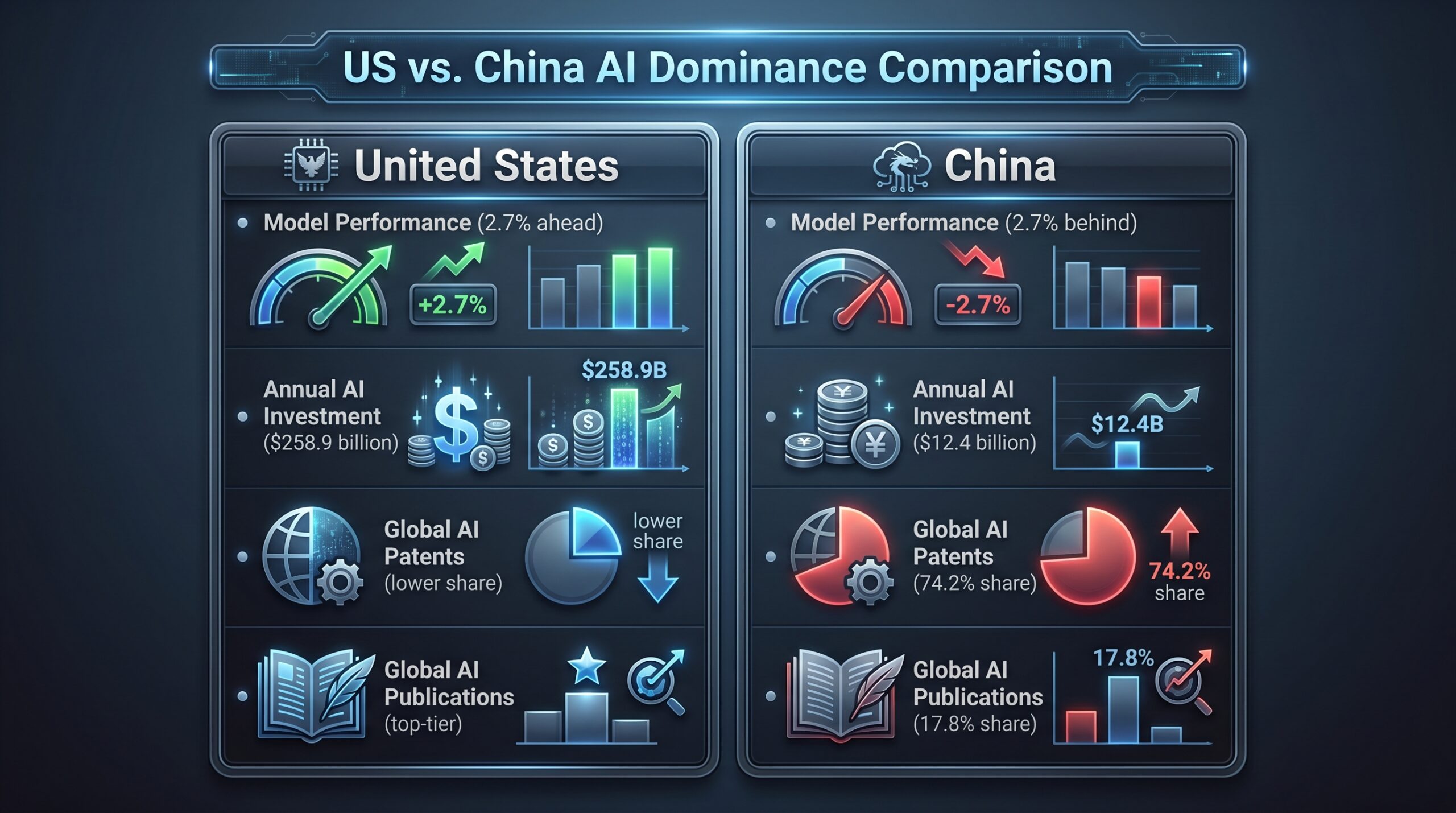

The US-China AI competition is intensifying. As of March 2026, China’s top AI models are now only 2.7% behind the leading US models on key benchmarks, a significant reduction from previous years. This accelerated convergence is validated by the recently published Stanford AI Index 2026 Report. The push is exemplified by new releases like DeepSeek V4, a Chinese model series launched in late April 2026 that directly targets the performance of OpenAI and Anthropic. Significantly, DeepSeek V4 leverages Huawei’s domestic chips, a key indicator of China’s strategic drive to build a sovereign AI stack independent of US-controlled technology supply chains.

TL;DR: US China AI Competition Update Key Insights

Key Updates on the US China AI Competition

- Performance Gap Closes: China’s best AI models now trail US counterparts by just 2.7% on key benchmarks (March 2026 data), a dramatic narrowing that changes the strategic calculus.

- DeepSeek V4 Launch: On April 23, 2026, Chinese AI lab DeepSeek launched preview versions of its flagship model, DeepSeek V4, in two variants: ‘Pro’ for high performance and ‘Flash’ for efficiency, demonstrating a focus on both raw power and practical deployment. (DeepSeek-V4: Million-Token Context for AI Agents)

- Hardware Realignment: DeepSeek V4’s use of Huawei chips, not Nvidia, is a direct response to US export controls and signals a successful pivot towards a domestically-sourced AI hardware foundation.

- Investment Disparity: The US outspent China in AI investment by a factor of 20-to-1 last year ($258.9 billion vs. $12.4 billion), making China’s performance gains an unexpected case of high capital efficiency.

- Research & IP Dominance: China holds an overwhelming 74.2% of global AI patents and accounts for 17.8% of AI publications, providing a deep research foundation for its applied model development.

- Containing Domestic Talent: Chinese authorities are actively preventing leading AI startups from relocating abroad for capital and markets, as seen with the Manus AI probe initiated on April 21, 2026.

- Multi-Layer Competition: The race is not winner-take-all but a sustained, parallel competition across different layers of the AI stack—models, hardware, talent—with each nation developing distinct strengths.

Key Takeaways from the US China AI Competition Update

Critical Decisions, Facts, and Implications in the AI Race

- The 2.7% Gap is a Tipping Point: This narrow margin means Chinese AI models are now functionally competitive for most commercial and research applications. It forces global enterprises to seriously evaluate Chinese AI providers as viable alternatives.

- Hardware Independence is Decoupling Global AI: DeepSeek V4 running on Huawei chips is not an isolated event. It represents the leading edge of a strategic effort to create a parallel, China-centric AI hardware and software stack, fracturing the previously US-dominated global ecosystem.

- Investment Alone Does Not Guarantee Leadership: The 20-to-1 spending advantage for the US has not prevented China from catching up. This means capital efficiency, research density, and integrated industrial policy are more powerful than previously assumed.

- Capital Flight is a New Frontline: China’s efforts to block AI startups from moving abroad, as evidenced by the Manus/Meta investigation, signals a shift from attracting foreign investment to actively containing domestic intellectual property and human capital.

- Long-Term Outlook is Sustained Parallelism: Expect both nations to continue advancing, but along diverging paths. The US will push the frontiers of raw model capability and emergent behaviors in an open ecosystem, while China will focus on vertically integrated, efficient, and sovereign AI solutions for domestic and aligned markets.

What is the US China AI Competition?

Defining the US China AI Race

The US-China AI competition is a multi-faceted strategic rivalry encompassing fundamental research, talent acquisition, private and public investment, hardware manufacturing, and real-world deployment of artificial intelligence technologies. It is driven by explicit national strategies to achieve technological supremacy, which is seen as the foundation for economic dominance, military advantage, and geopolitical influence in the 21st century.

Understanding this competition is crucial for businesses, policymakers, and technologists alike. It impacts everything from supply chain resilience to ethical AI development. The stakes are global, influencing the future landscape of innovation and power dynamics.

What Most People Get Wrong About the US China AI Competition

Many observers incorrectly view this as a zero-sum, winner-take-all sprint. This is a dangerous oversimplification. The reality, as of April 2026, is sustained, parallel competition across different layers of the stack.

The US maintains deep leads in foundational model architecture and venture-scale investment. China, meanwhile, has surged ahead in patent generation, publication volume, and now in creating integrated hardware-software packages like DeepSeek V4 on Huawei chips. This layered competition means both nations can achieve leadership in different aspects of AI.

Another major misconception is that massive investment guarantees superior outcomes. The data disproves this: the US spent over $258 billion to achieve a 2.7% performance lead, while China spent $12.4 billion to achieve near-parity. This demonstrates that China’s focus on applied research and a directed, state-backed industrial strategy may achieve different, but equally significant, forms of leadership.

It’s not just about who spends more, but how effectively that capital is deployed and integrated into a national strategy. China’s approach highlights the power of coordinated industrial policy.

Why the US China AI Competition Matters Now

Current Attention and Geopolitical Stakes of US China AI

The competition matters uniquely in Q2 2026 because the gap in core model performance has nearly vanished. A 2.7% difference is within the margin of error for many real-world business applications. This means decisions made today about AI adoption, partnerships, and supply chains will have long-term strategic implications.

Geopolitically, AI is now central to national security doctrines, with both nations embedding AI into defense systems, cyber operations, and intelligence analysis. The race determines which set of standards, ethics, and technological architectures will shape the global digital future. The implications extend to international relations and alliances.

Market Shifts and Behavior Changes in the AI Landscape

The competition is driving concrete market realignments right now. Investors are rotating capital from traditional US tech stocks into Chinese semiconductor firms, betting on the growth of the sovereign AI stack. This shift reflects a recognition of China’s growing self-sufficiency in critical AI hardware.

In China, AI startups are facing increased scrutiny and regulatory hurdles if they attempt to incorporate offshore or seek funding abroad, as seen with the Manus case. Conversely, the US is doubling down on export controls, inadvertently accelerating China’s domestic innovation cycle. For global operators, this means supply chains are bifurcating, creating two potential technology sourcing paths with different compliance, performance, and vendor risks. Preparing for this dual ecosystem is becoming a business imperative.

How the US China AI Competition Works: Mechanics of the Race

Understanding the Different Layers of AI Competition

The race operates across five interconnected dimensions:

- Research & Development (R&D): This is the foundation. China’s dominance in patents (74.2%) and strong showing in publications (17.8%) provides a massive reservoir of ideas and intellectual property. The US focuses more on breakthrough research published in top-tier conferences, which often precedes commercial model development.

- Talent Acquisition & Retention: The US has historically attracted global AI talent to its universities and companies. In 2026, China is countering by aggressively retaining its top graduates and preventing startup founders from leaving, aiming to create a closed loop of domestic expertise.

- Investment Strategies: The US model relies on massive private venture capital and corporate R&D ($258.9B). China’s model blends smaller, more directed private investment ($12.4B) with significant state-backed funding for national champions and strategic projects, leading to high capital efficiency.

- Hardware: The core physical layer. US export controls on advanced Nvidia chips (A100, H100, H200) were intended to slow China. The effect has been to catalyze China’s domestic chip industry, with Huawei’s Ascend series now powering frontier models like DeepSeek V4. (Google TPU 8t and 8i: Eighth Generation AI Chips for Agents offer alternative perspectives from a US vendor).

- Model Development & Deployment: The most visible layer. US companies (OpenAI, Anthropic) race to build larger, more capable general-purpose models. Chinese companies (DeepSeek) are building similarly powerful models but with a keen focus on efficiency, cost, and integration with domestic hardware—optimizing for deployment at scale within their controlled ecosystem. (OpenAI’s Latest Models Explained: GPT-5.5, GPT-Rosalind, and Agents SDK Updates provide insight into US model development).

Strategic Responses to US Export Controls

US export controls were a strategic shock to China’s AI ecosystem. The response was not attrition but aggressive innovation. The "Sovereign AI Stack" strategy emerged, mandating the development of a fully domestic pipeline from silicon design and fabrication to compiler software, AI frameworks, and end-user models.

DeepSeek V4 on Huawei chips is the first major, publicly acknowledged success of this strategy. Huawei’s hardware, combined with China’s proprietary frameworks like MindSpore, creates a walled technology garden that is immune to future US sanctions. This decoupling means the global AI market is segmenting into two distinct technological spheres. Businesses must now strategically choose between or integrate with these diverging ecosystems. This mirrors some of the concerns seen with the strategic dependencies relevant to OpenAI WebSockets Boost Agentic AI Workflows, albeit on a larger geopolitical scale.

Real-World Examples & Use Cases in the US China AI Competition

DeepSeek V4: A Game-Changer in Chinese AI Models

DeepSeek V4, launched on April 23, 2026, represents a tangible leap in China’s competitive posture. It’s not just the model’s performance—reportedly within single-digit percentages of GPT-4 Turbo and Claude 3.5 Sonnet on the Arena benchmark—but its architecture and supply chain that matter.

The model is explicitly designed to run optimally on Huawei’s Ascend AI processors. For enterprise clients within China and in markets like Southeast Asia and the Middle East, DeepSeek V4 offers a high-performance AI solution without the geopolitical risk or licensing complexities associated with US technology. Its two versions, Pro and Flash, also signal a focus on segmenting the market: the Pro version targets top-tier research and complex reasoning, while the Flash version is optimized for high-volume, cost-sensitive applications like customer service automation and content moderation. This diversified approach makes it a formidable competitor, similar to how OpenAI’s new models aim for broad applicability.

Huawei’s Role in China’s Sovereign AI Stack

Huawei has transformed from a telecommunications giant to the linchpin of China’s AI independence. Following its placement on the US Entity List, Huawei poured resources into its HiSilicon chip design unit and the Ascend AI compute platform. The successful integration of these chips with DeepSeek V4 proves the stack works.

Use cases extend beyond model training: Huawei is deploying Ascend-based AI servers in Chinese data centers for smart city infrastructure, industrial IoT analytics, and telecommunications network optimization. This creates a closed loop where domestic demand fuels domestic hardware advancement, which in turn enables better domestic software, further insulating the ecosystem. This integrated strategy showcases a powerful shift in industrial development.

AI Patent Dominance and Research Output

The sheer volume of Chinese AI patents (74.2% global share) translates into practical advantages. These patents cover countless incremental improvements in algorithms, chip architectures, sensor fusion, and application interfaces.

For example, Chinese companies hold dense patent portfolios in computer vision for manufacturing quality control and facial recognition—technologies that are then rapidly deployed at scale in factories and public security systems. The high volume of publications (17.8% share) ensures a constant flow of research talent and novel ideas into the commercial pipeline, allowing Chinese firms to quickly adopt and implement the latest global research trends, often with a focus on practical engineering and optimization. This rapid application of research into practical tools is a key strength.

Comparing US and China’s AI Dominance

AI Model Performance: US vs. China AI Models

The Stanford AI Index 2026 benchmark data confirms the narrative: China has caught up in model capability. A 2.7% performance gap means that for the vast majority of enterprise tasks—code generation, document summarization, customer support—the choice between a leading US model and a leading Chinese model is no longer about capability but about ecosystem, compliance, cost, and latency. For instance, while GPT-5.5 Now Available in GitHub Copilot for Enterprise Users, Chinese alternatives offer different benefits to local markets.

DeepSeek V4-Pro is positioned to compete directly with OpenAI’s o1 series and Anthropic’s Claude 3.5 Sonnet for complex reasoning tasks. The Flash version competes in the high-efficiency segment against models like GPT-4o-mini. This suggests a mature and competitive market for AI models.

Investment vs. Innovation: US AI Spending vs. China’s Efficiency

The investment disparity is staggering but misleading as a sole metric. The US’s $258.9 billion funds a sprawling ecosystem of startups, moonshot projects, and corporate R&D, with high tolerance for failure in pursuit of breakthroughs. China’s $12.4 billion is more narrowly focused on applied problems, commercialization, and technologies with clear military or industrial utility.

This focus, combined with top-down coordination and pressure to utilize domestic resources, yields exceptional capital efficiency. China isn’t necessarily inventing the Transformer architecture, but it is perfecting its implementation and building it on homemade silicon at a fraction of the cost. This strategic allocation of resources distinguishes its approach.

DeepSeek V4 Variants Comparison

DeepSeek V4 offers two distinct variants, demonstrating a strategic approach to market segmentation:

- DeepSeek-V4-Pro: Designed for maximum reasoning capability and raw performance, targeting top-tier US models like OpenAI’s o1 series and Claude 3.5 for complex R&D and advanced coding tasks. It has a higher computational cost per query.

- DeepSeek-V4-Flash: Optimized for efficiency and cost-effectiveness, suitable for high-volume, latency-sensitive applications like enterprise chatbots and real-time translation. It boasts lower latency and cost per query for practical deployment.

This dual approach allows DeepSeek to address both the high-performance and high-efficiency segments of the AI market effectively.

| Metric | United States | China | Source/Context |

|---|---|---|---|

| AI Model Performance Gap | 2.7% ahead of China’s best | 2.7% behind the US’s best | Stanford AI Index 2026 Report (as of March 2026) |

| Annual AI Investment (Last Year) | $258.9 billion | $12.4 billion | From Stanford AI Index, cited by multiple outlets |

| Global AI Patents | Significantly lower share | 74.2% of global patents | CIW.news report |

| Global AI Publications | Leading in top-tier conference papers | 17.8% of global publications | CIW.news report |

| Feature | DeepSeek-V4-Pro | DeepSeek-V4-Flash |

|---|---|---|

| Primary Focus | Maximum reasoning capability & performance | Efficiency & cost-effectiveness |

| Performance Level | Targets top-tier US models (OpenAI o1, Claude 3.5) | Competitive for high-volume, latency-sensitive tasks |

| Efficiency | Higher computational cost per query | Optimized for lower latency and cost per query |

| Use Case Fit | Complex R&D, strategic analysis, advanced coding | Enterprise chatbots, real-time translation, content generation |

Tools, Vendors, and Implementation Paths in the US China AI Race

Key AI Technologies and Vendors from Both Nations

US-Centric Ecosystem:

- Models: OpenAI (GPT-4o, o1 series, and advanced models like GPT-5.5), Anthropic (Claude family), Google (Gemini), Meta (Llama). These continue to push the boundaries of general-purpose AI.

- Hardware: Nvidia (H100, H200, Blackwell), AMD (MI300X), and cloud vendors (AWS Trainium/Inferentia, Google TPU like the Google TPU 8t and 8i). The US remains a leader in high-performance AI accelerators.

- Infrastructure: Reliant on global supply chains (TSMC in Taiwan, ASML in EU) for advanced chip fabrication. This global dependency presents both strengths and vulnerabilities.

China-Centric (Sovereign) Ecosystem:

- Models: DeepSeek (V4 Pro/Flash, like the DeepSeek-V4: Million-Token Context for AI Agents), Baidu (Ernie), Alibaba (Qwen), Zhipu AI (GLM). These models are deeply integrated into China’s digital economy.

- Hardware: Huawei (Ascend series), Cambricon, Biren Technology, and domestic foundries like SMIC. China is rapidly building its capacity for indigenous AI hardware.

- Infrastructure: Increasingly reliant on domestic chip fabrication (SMIC’s 7nm/5nm class nodes) and homegrown AI frameworks (Baidu’s PaddlePaddle, Huawei’s MindSpore). This aims for complete self-sufficiency.

The critical trade-off is between performance and sovereignty. Choosing the US ecosystem offers access to the current performance frontier and a vibrant global developer community but comes with potential regulatory risks (export controls, data privacy laws). Choosing the China ecosystem offers insulation from Western sanctions and deep integration with the Chinese market but may involve navigating different standards, less mature tooling, and potential performance ceilings set by domestic hardware. Understanding these trade-offs is vital for global businesses.

Implementation Paths: Sovereign AI vs. Open Ecosystems

Path 1: Sovereign AI Implementation (China’s Model)

- Pro: Complete control over the technology stack; immunity to foreign sanctions; data stays within jurisdictional boundaries; optimized for domestic policy goals.

- Con: Risk of technological isolation; potentially slower adoption of global breakthroughs; higher initial costs for duplicate R&D; vendor lock-in to domestic champions.

- Implementation Checklist:

- Mandate use of domestic AI chips (Huawei Ascend) in all government and critical infrastructure projects.

- Subsidize the development and adoption of domestic AI frameworks (MindSpore, PaddlePaddle).

- Create regulatory sandboxes that favor applications built on the sovereign stack.

- Fund large-scale, national AI model training projects on domestic infrastructure.

- Implement data localization laws that make using foreign AI services legally or practically difficult.

Path 2: Open Ecosystem Implementation (US Model)

- Pro: Access to a global market of best-in-class components; rapid innovation through intense competition; ability to attract global talent; strong venture capital funding model.

- Con: Strategic dependencies on foreign supply chains (e.g., Taiwan for chips); vulnerability of critical technology to geopolitical disputes; potential for regulatory fragmentation.

- Implementation Checklist:

- Use export controls and investment screening to protect core technologies.

- Fund basic research at universities and national labs to maintain a lead in foundational science.

- Fostering public-private partnerships for grand challenges (e.g., biosecurity, climate AI).

- Advocate for open standards and interoperable frameworks to maintain global influence.

- Leverage alliances (with EU, Japan, South Korea) to build resilient, allied technology networks.

AI Implementation Paths: Sovereign vs. Open Ecosystems

- Sovereign AI (China’s Model)

– Pros: Control, immunity to sanctions, data localization, policy alignment

– Cons: Isolation risk, slower adoption of global breakthroughs, high R&D costs, vendor lock-in

– Key Actions: Mandate domestic chips/frameworks, subsidies, regulatory sandboxes, national model training, data localization - Open Ecosystem (US Model)

– Pros: Global component access, rapid innovation, talent attraction, VC funding

– Cons: Supply chain dependencies, geopolitical vulnerability, regulatory fragmentation

– Key Actions: Export controls, basic research funding, public-private partnerships, open standards advocacy, alliance building

Costs, ROI, and Monetization Upside in US China AI Competition

Investment Costs and Economic Impact of the AI Race

The cost of participation is astronomical. The US’s $258.9 billion annual spend goes towards GPU clusters (a single Nvidia H100 server can cost over $200,000), sky-high engineer salaries, and massive cloud compute bills for model training that can exceed $100 million per run. While US companies like OpenAI offer advanced models (OpenAI’s Latest Models Explained: GPT-5.5), the development cost is substantial.

China’s lower stated investment of $12.4 billion belies significant indirect subsidies, state-backed low-interest loans to chip fabs, and the opportunity cost of directing top engineering talent to national projects. The economic impact is measured in more than dollars.

It’s about GDP growth through productivity gains, securing high-value future industries (biotech, autonomous systems), and the incalculable strategic value of military AI superiority. China’s approach seeks ROI through vertical integration: controlling the chips, the models, and the applications ensures that economic value is captured domestically across the entire value chain. Early data suggests this integrated approach yields a higher ROI on R&D spending in terms of immediate industrial application.

Monetization Upside and Revenue Generation in AI

US companies monetize primarily through enterprise SaaS subscriptions (e.g., OpenAI API, Microsoft Copilot, GitHub Copilot), cloud compute rentals (AWS, Google Cloud), and hardware sales (Nvidia). The model is to sell access to the most advanced general-purpose intelligence. This has a global reach but faces increasing competition.

Chinese companies are monetizing through deeply embedded industry-specific solutions. For example, DeepSeek’s models are being packaged by Alibaba Cloud and Tencent Cloud not as raw APIs, but as complete solutions for smart manufacturing, supply chain logistics, and financial risk analysis that run on domestic hardware. The monetization upside for China lies in selling digital transformation to its massive industrial base and exporting integrated AI infrastructure packages to countries aligned with its Belt and Road Initiative, offering a sanction-resistant alternative to Western tech. This strategy offers significant long-term revenue potential tied to national and allied markets.

Risks, Pitfalls, and Myths vs. Facts in the US China AI Competition

Key Risks and Pitfalls in the AI Race

Risks:

- Technological Fragmentation & Incompatibility: The development of separate AI stacks could lead to a "splinternet" for AI, where models, data formats, and APIs are not interoperable, stifling global scientific collaboration and business efficiency.

- Supply Chain Over-correction: Over-reliance on domestic supply chains can lead to inefficiency and technological lag. China’s semiconductor manufacturing, while advanced, still trails global leaders in yield and transistor density for the most cutting-edge chips.

- Escalation & Miscalculation: Military integration of AI increases the risk of rapid escalation in a crisis. Automated cyberdefense or drone swarms could trigger responses faster than human diplomats can manage.

- Innovation Stagnation in Closed Ecosystems: China’s sovereign stack risks insulating its researchers from the most creative, disruptive ideas that often emerge from the global open-source community and academic freedom.

Risk Mitigation Checklist for Global Enterprises:

- Dual-Sourcing Strategy: Evaluate critical AI workloads for viability on both US and Chinese model/hardware platforms.

- Compliance Forensics: Continuously monitor evolving US export control lists (EAR) and Chinese data security laws (DSL) to avoid legal pitfalls.

- Talent Diversification: Build teams with experience in both Western (PyTorch, TensorFlow) and Chinese (PaddlePaddle, MindSpore) development frameworks. This includes understanding platforms that support specific AI tasks, such as OpenAI Codex for coding.

- Scenario Planning: Run war-game exercises for scenarios involving sudden denial of service from a primary AI vendor due to geopolitical sanctions.

- Invest in Abstraction Layers: Use middleware and API gateways that can, where possible, route requests to different model backends to maintain operational flexibility. This is crucial for managing geopolitical tech divides.

Myths vs. Facts: Unpacking US China AI Hype

- Myth: The US will maintain an unassailable lead due to its innovation culture and venture capital.

Fact: The 2.7% performance gap proves this is false. China has demonstrated it can achieve near-parity through focused, state-coordinated effort, even with vastly less direct investment. - Myth: China merely copies Western AI technology and cannot truly innovate.

Fact: While China benefits from open global research, its dominance in patents (74.2%) and its engineering of a complete, homegrown AI stack from chips to models (DeepSeek V4 on Huawei) is a formidable innovation in systems integration and industrial policy. - Myth: This is a race with a single winner who will dominate global AI.

Fact: The competition is evolving into sustained, parallel competition across different layers of the stack. The US may lead in frontier model capabilities, while China leads in deployment scale, hardware integration, and certain applied fields. Two distinct, competing technological ecosystems are likely to persist. - Myth: High investment directly translates to better AI models.

Fact: The US spends 20x more for a 2.7% lead, revealing diminishing returns at the frontier. China’s model of directed research, talent retention, and vertical integration is a more capital-efficient path to competitive AI, at least in the near term. This also applies to fields like Best AI Crypto Trading Bots 2026, where efficiency and strategic deployment can outweigh sheer computational power.

Frequently Asked Questions About the US China AI Competition Update

Here are answers to common questions about the current state of US-China AI competition in 2026.

How close is China’s AI model performance to the US?

As of March 2026, measured by the Stanford AI Index, China’s top AI models are only 2.7% behind the leading US models on aggregate benchmarks. This narrow gap indicates Chinese models are now functionally competitive for the vast majority of commercial and research applications, a significant shift from just two years ago.

What is DeepSeek V4 and why is it significant for the US China AI competition?

DeepSeek V4 is a flagship AI model series launched by a Chinese lab in April 2026. Its significance is two-fold: it demonstrates performance rivaling top US models like those from OpenAI and Anthropic, and it is built to run on Chinese-made Huawei chips. This marks a major step in China’s "Sovereign AI Stack" strategy, reducing critical dependency on US-controlled hardware. You can learn more about its capabilities at DeepSeek-V4: Million-Token Context for AI Agents.

How do US and China compare in AI investment?

The disparity remains vast. In the last year, the US invested an estimated $258.9 billion in private AI funding and corporate R&D, while China invested $12.4 billion. The shock is that despite this 20-to-1 spending disadvantage, China has nearly closed the model performance gap, suggesting a much higher degree of capital efficiency and focused application of resources.

Does China dominate in any specific areas of AI development?

Absolutely. China holds a commanding 74.2% of all global AI patents, indicating a massive focus on protecting incremental and applied innovations. It also accounts for 17.8% of global AI publications, showing deep engagement in foundational research. These strengths provide a powerful substrate for its rapid advances in commercial models.

What is a ‘Sovereign AI Stack’ and why is China pursuing it?

A Sovereign AI Stack is a national strategy to control every critical layer of AI technology—from the design and fabrication of semiconductors (chips) to the software frameworks and the final AI models—using domestically developed and controlled resources. China is pursuing this aggressively in direct response to US export controls on advanced chips, aiming to ensure its AI development is immune to foreign sanctions and aligns with its national security and industrial policy goals. This is a critical factor influencing the global technology landscape.

Glossary of US China AI Competition Terms

Key Definitions for Understanding the AI Race

- DeepSeek V4: A new series of state-of-the-art AI models released by Chinese AI laboratory DeepSeek in April 2026. It is available in two main versions: "DeepSeek-V4-Pro" for high-performance tasks and "DeepSeek-V4-Flash" as a more efficient, economical variant. Its development and operation on Huawei chips is a central case study in China’s sovereign AI strategy. For more details, see DeepSeek-V4: Million-Token Context for AI Agents.

- Arena benchmark: A widely recognized, crowd-sourced evaluation platform used to rank and compare the performance of leading large language models (LLMs). The Stanford AI Index 2026 report uses data from such benchmarks to quantify the 2.7% performance gap between the US and China.

- Sovereign AI Stack: A comprehensive national strategy to develop and control an entire, integrated AI technology ecosystem domestically. This includes indigenous hardware (e.g., Huawei chips), software frameworks (e.g., MindSpore), and AI models (e.g., DeepSeek). Its goal is to eliminate strategic dependencies on foreign technology and ensure self-sufficiency.

- AI Index Report: An annual comprehensive report published by Stanford University’s Institute for Human-Centered Artificial Intelligence (HAI). It provides data and analysis on trends in AI, including technical performance, investment, and geopolitical dynamics. The 2026 edition is a primary source for current US-China competition metrics.

- Export Controls: Legal restrictions imposed by a government, particularly the United States through the Export Administration Regulations (EAR), on the sale, transfer, or re-export of specific technologies—such as advanced AI accelerator chips designed by Nvidia and AMD—to certain countries or entities, notably China. These controls are a primary driver behind China’s push for a sovereign AI stack.

References for US China AI Competition Update

Cited Sources for the US China AI Competition

The factual data and analysis in this report are synthesized from the following sources, which reflect the latest reporting and research as of April 2026:

- Stanford University, Institute for Human-Centered AI (HAI). AI Index Report 2026. Provides the core competitive metrics: the 2.7% AI model performance gap (as of March 2026) and the $258.9 billion (US) vs. $12.4 billion (China) investment figures.

- Futurism, El-Balad.com, The Next Web, CIW.news. Reporting (April 2026) on the findings of the Stanford AI Index 2026 regarding the narrowing US-China AI performance gap.

- Ogun Security, Enterprise AI Economictimes. Reports and technical announcements (late April 2026) detailing the launch of DeepSeek V4, its "Pro" and "Flash" versions, and the latter’s design for efficiency and economy. This aligns with trends observed in models like DeepSeek-V4: Million-Token Context for AI Agents.

- Swisher Post, RSWebSols, South China Morning Post (SCMP). Exclusive reports (April 2026) confirming that DeepSeek V4 utilizes Huawei’s Ascend AI chips, highlighting the strategic shift from Nvidia.

- CIW.news. Reporting on China’s global leadership in AI patents (74.2% share) and significant contribution to AI publications (17.8% share).

- The Washington Post. Report dated April 21, 2026, detailing Chinese government scrutiny of AI startup Manus as it attempted to relocate abroad after acquisition by Meta, exemplifying efforts to retain domestic AI talent and companies.

This article, dated April 26, 2026, consolidates these recent developments into a comprehensive guide for understanding the current state and immediate trajectory of the US-China AI competition.